Cross-border peer-to-peer (P2P) payments, often synonymous with remittances, have long been a cornerstone of global economies, enabling individuals to send money to family and friends across international borders. However, this vital process has historically been plagued by inefficiencies: high transaction fees, slow processing times, opaque exchange rates, and a lack of accessibility for unbanked populations. Enter blockchain technology, a disruptive force poised to fundamentally transform how cross-border P2P payments are conducted.

Blockchain, the decentralized and immutable ledger system famously underpinning cryptocurrencies like Bitcoin, offers a compelling solution to many of the long-standing challenges in the remittance landscape. Its inherent characteristics directly address the pain points of traditional money transfer systems, paving the way for a more efficient, equitable, and accessible future for global payments.

The Traditional Landscape: A Web of Intermediaries

Before delving into blockchain’s impact, it’s crucial to understand the traditional remittance ecosystem. When an individual sends money internationally through a bank or a money transfer operator (MTO) like Western Union or MoneyGram, the funds typically pass through a series of intermediaries. This often involves correspondent banks, payment networks, and local agents, each taking a cut for their services. This multi-layered process results in:

- High Fees: Each intermediary adds a fee, cumulatively making cross-border transfers expensive, especially for smaller amounts.

- Slow Speeds: Settlement can take days, as funds move between different financial institutions and across various time zones.

- Lack of Transparency: Senders and receivers often have limited visibility into the exact exchange rates and fees applied until the transaction is complete.

- Exclusion: A significant portion of the global population remains unbanked, making it difficult or impossible for them to access traditional remittance services.

Blockchain’s Disruptive Influence: Key Impacts

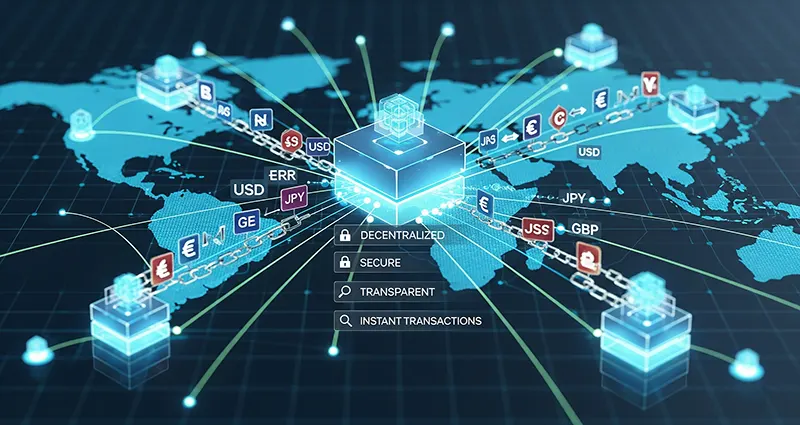

Blockchain technology offers a paradigm shift by streamlining this complex process, primarily through decentralization and cryptographic security.

1. Reduced Transaction Costs:

The most immediate and significant impact of blockchain on cross-border P2P payments is the drastic reduction in transaction fees. By eliminating the need for multiple intermediaries, blockchain-based platforms can facilitate direct transfers between sender and receiver. Cryptocurrencies and stablecoins, built on blockchain, allow for value transfer with minimal network fees, often just fractions of a cent, regardless of the amount being sent. This means more money reaches the intended recipient, a critical factor for families relying on remittances.

2. Accelerated Transaction Speeds:

Traditional bank transfers can take days to clear due to batch processing and interbank reconciliation. Blockchain transactions, once validated by the network, are typically confirmed and settled within minutes, or even seconds, depending on the specific blockchain. This near-instantaneous settlement provides unparalleled speed, especially beneficial in urgent situations where timely access to funds is crucial.

3. Enhanced Transparency and Security:

Every transaction on a public blockchain is recorded on an immutable ledger, visible to all participants on the network (though sender/receiver identities are typically pseudonymous). This inherent transparency means senders and receivers can track their funds in real-time, from initiation to completion, without relying on external updates. Cryptographic encryption further ensures the security and integrity of each transaction, significantly reducing the risk of fraud and tampering.

4. Financial Inclusion for the Unbanked:

One of blockchain’s most profound impacts is its potential to foster financial inclusion. Many blockchain-based payment solutions only require a smartphone and internet access, bypassing the need for a traditional bank account This opens up cross-border payment avenues for the estimated 1.7 billion unbanked adults globally, allowing them to participate in the global economy and send/receive funds with ease. This can be particularly transformative in developing regions where banking infrastructure is limited.

5. Stablecoins and Reduced Volatility:

While early blockchain payments faced challenges due to the volatility of cryptocurrencies, the emergence of stablecoins has provided a crucial solution. Stablecoins are cryptocurrencies pegged to a stable asset, like the US dollar, minimizing price fluctuations. This allows users to send value across borders using a digital asset that maintains its purchasing power, mitigating the risks associated with volatile cryptocurrencies while retaining the benefits of blockchain technology.

6. Programmable Payments and Smart Contracts:

Blockchain’s ability to support smart contracts adds another layer of innovation. These self-executing contracts can automate payment conditions, such as releasing funds only when certain criteria are met. While more complex for simple P2P remittances, this feature holds immense potential for future applications, such as conditional aid disbursements or automated recurring payments, adding flexibility and trust to transactions.

Challenges and the Road Ahead

Despite its revolutionary potential, blockchain adoption for cross-border P2P payments still faces challenges. Regulatory uncertainty, scalability issues for some blockchain networks, user experience complexities, and the need for greater public education are hurdles that must be overcome.

However, as the technology matures, regulatory frameworks evolve, and user-friendly interfaces become more prevalent, blockchain is set to solidify its role as the backbone of future cross-border P2P payments. By offering a faster, cheaper, more transparent, and inclusive alternative to traditional methods, blockchain technology is not just impacting remittances—it’s redefining them, empowering individuals and fostering greater global economic connectivity.